What Autumn Budget 2025 Means for Every Stage of Life

- Nov 27, 2025

- 8 min read

Updated: Dec 4, 2025

The Autumn Budget 2025 brings a number of tax, pension and savings-rule changes that will ripple through people’s finances, depending on their stage of life.

At Brancaster House Financial Planning, we believe financial planning should evolve with each life stage. Here’s how the new budget could impact different kinds of clients - and where a tailored plan matters more than ever.

Key Highlights from the Autumn Budget 2025

Before diving into life-stages, here are the main headline changes to be aware of:

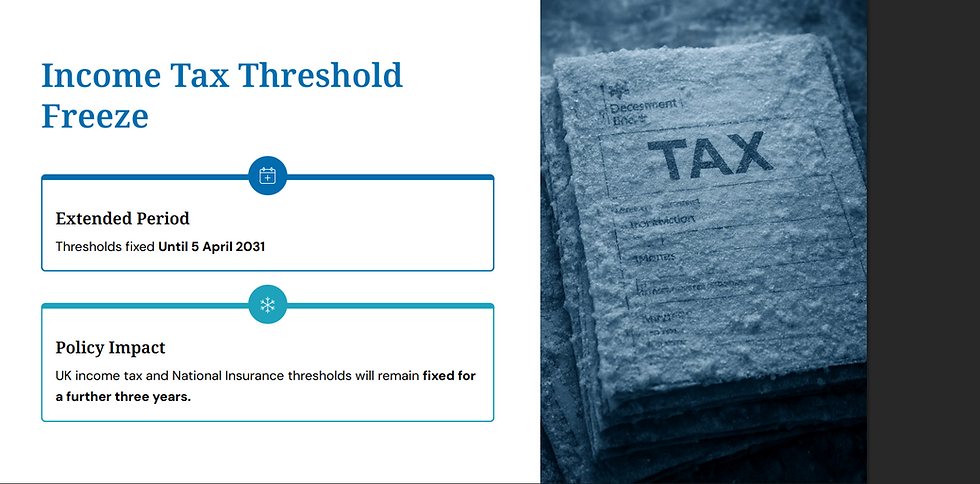

Income-tax thresholds (personal allowance, higher-rate thresholds) and National Insurance thresholds have been frozen until April 2031.

Salary-sacrifice pension contributions that benefit from NI exemption will now be capped at £2,000 per year from April 2029.

Tax and National Insurance treatment of pension contributions above that cap will change - meaning some savers may end up worse off if they don’t plan carefully.

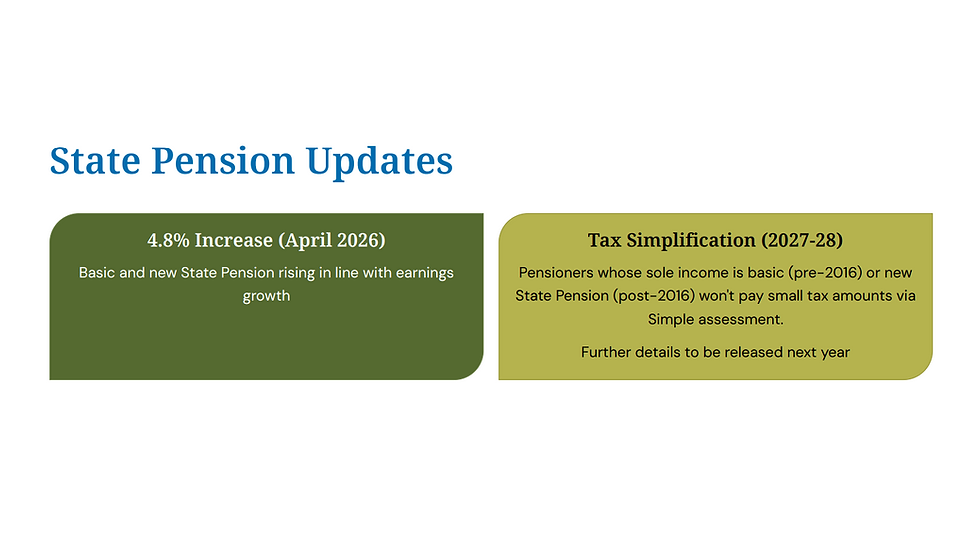

For pensioners, the State Pension will rise by 4.8% from April 2026 under the Triple-Lock rule.

Other changes affecting savings, investments, property income and allowances (e.g. cash-savings usage, investment strategies, tax on unearned income) were also outlined.

These changes affect almost everyone but the impact and what you should do will vary, depending on where you are in the life journey.

Young People & Early Career

What might change for you

With tax thresholds frozen, as your income grows over time you may find yourself pushed into higher tax bands sooner than expected; a phenomenon often dubbed “fiscal drag.” That means take-home pay grows more slowly unless your raises outpace inflation.

For those starting to save, the pension salary-sacrifice cap may reduce long-term pension benefits if you don’t adjust your savings strategy.

Savings and investment decisions become more important. Traditional cash-savings may yield less value long-term if inflation and tax pressures continue; starting to build a diversified savings/investment portfolio early could pay off.

What you should consider doing now

Review how much you’re contributing to pensions and consider alternative methods if salary sacrifice becomes less efficient.

Start investing early where feasible: even small investments over time benefit from compounding.

Build an emergency fund with tax-efficient options where possible (e.g. ISAs, diversified savings), but also consider investing intelligently for long-term growth.

Make full use of your ISA allowance (even with the recent changes) to help reduce tax on interest through Cash ISAs and on dividends and investment growth through Stocks & Shares ISAs.

Families & Mid-Career

What might change for you

Household income growth may be taxed more heavily over time due to frozen thresholds - putting pressure on budgeting and long-term savings goals.

With pension salary-sacrifice becoming less attractive beyond £2,000, using other retirement-saving vehicles or adjusting contribution strategies will be important.

Raising children, mortgage payments, and other costs may squeeze disposable income; so efficient tax and savings planning becomes more important than ever.

ISA allowances remain frozen, meaning families can save less tax-free each year in real terms, pushing more households into paying tax on their savings and reducing long-term wealth-building potential.

What to do now

Review and possibly recalibrate pension contributions.

Build a balanced savings and investment plan that considers long-term goals (education, property, retirement).

Take advantage of any spousal or household-level tax-efficient strategies (joint pensions, diversified savings, allowances).

Consider scheduling a review of your financial plan' factoring in the new tax regime, growth ambitions, family goals and retirement plans.

Business Owners & Entrepreneurs

What might change for you

The frozen tax thresholds and changes to pension contribution rules will impact both personal and business financial planning, especially if you pay yourself via salary or dividends.

If your business pays into a pension via salary sacrifice for you or staff, the £2,000 cap may reduce the benefit - so business and remuneration planning will need revisiting.

Growth plans, reinvestment strategies, and long-term business exits or succession plans may need adjusting to account for changes in tax, pension and savings rules.

What to do now

Re-evaluate business remuneration structure - salary vs dividends vs pension contributions - in light of changes.

Consider involving a financial planner early to align business growth ambitions, tax efficiency, personal finances, and retirement planning.

Review long-term plans for business exit, sale, or hand-over - and how changes in pensions, tax bands, and allowances might affect these.

Property, Homeowners & Investors

The Autumn Budget 2025 didn’t just affect pensions, income tax and savings - it also introduced several measures that will reshape the property market. Whether you’re a homeowner, a first-time buyer, or a property investor, it’s worth understanding how the changes could impact you now and over the next few years.

Key Property-Related Budget Changes

The Budget confirms a new “mansion tax” - a High Value Council-Tax Surcharge - on homes valued over £2 million, payable from April 2028. Homes in that bracket will face an additional annual surcharge on top of regular council tax, ranging from £2,500 up to £7,500, depending on the property’s value.

For property investors and landlords: from April 2027, income from property rentals will face a 2 percentage-point increase in income tax rates, raising the basic, higher and additional rates to 22%, 42% and 47% respectively.

Stamp Duty remains unchanged for now. The government confirmed no reforms to the existing Stamp Duty Land Tax (SDLT) thresholds in this Budget.

First-Time Buyers & Prospective Homeowners

If you’re thinking of buying your first home or moving up the ladder - here’s what to keep in mind:

No Stamp Duty changes in this Budget means the usual tax costs at purchase remain the same (unless future Budgets intervene). That gives some short-term certainty.

Even with stable Stamp Duty, the wider economic backdrop (tax rises elsewhere, income-tax thresholds frozen, more pressure on landlords) may impact demand, lending rates and mortgage costs - which could influence buyer behaviour.

If you plan to stay in your home long-term, mortgage affordability and future property tax incentives are now more important than ever - so make sure you model your costs over 5–10 years, not just immediate expenses.

What to do now:

Get a realistic long-term affordability plan - account for potential rate changes, cost-of-living pressures, and future property taxes.

Consider locking in fixed-rate mortgages if possible to avoid volatility.

Prioritise building an emergency fund - and consider diversifying savings/investments rather than relying solely on property value growth.

Homeowners (Owner-Occupied)

For people who already own their home and are settled, the Autumn Budget brings some new considerations - especially for higher-value properties

If your home is valued over £2 million and you’re in England, be aware that the new mansion tax surcharge will apply from April 2028. That could increase annual housing costs significantly.

For most “average” homeowners this won’t apply — the surcharge is aimed at the top 1% of properties.

However, higher taxes on rental and investment property income could still ripple through the wider property market — potentially impacting demand, home values, and resale dynamics over the long term.

What to do now:

If you own a high-value property, run cash-flow forecasts now with the potential surcharge included - and consider what a £2,500–£7,500 annual extra cost means for your long-term plans.

If you expect to sell or downsize in the next few years - plan with potential market shifts in mind (demand, valuations, buyer behaviours).

If your property is more modest - still think long-term: economic headwinds and policy changes could influence house prices broadly, so make sure your home-ownership isn’t overleveraged.

Property Investors & Landlords

If you own rental properties or investment housing, the Budget brings several direct implications:

From April 2027, rental income will be taxed at higher rates - basic 22%, higher 42%, additional 47%. That reduces net yield for many landlords.

With higher tax burdens, some landlords may re-evaluate their portfolios - potentially selling properties or transferring them to companies. This could impact rental supply and property values long-term. Analysts are already warning this may push house price growth down.

The new “mansion tax” won’t directly hit most buy-to-let investors (since it targets owner-occupied high-value homes), but the general tax and regulatory climate - plus increased costs - may make property investment less attractive overall.

What to do now:

Review your rental yields and cash flow projections now, factoring in the higher income-tax rates from 2027.

Consider whether buy-to-let remains a viable long-term strategy - or whether other investment vehicles (e.g. equities, diversified portfolios) now offer better risk/return.

If you plan to sell or restructure, get professional tax/financial advice early -especially if you also run a business or have complex personal finances.

Why It Matters - And How Professional Planning Helps

The property changes introduced in Autumn Budget 2025 aren’t minor tweaks - for many people, they represent a material shift in long-term housing costs, investment returns or retirement security.

At Brancaster House Financial Planning, we believe property should be part of a holistic financial plan - not a stand-alone asset you hope will keep growing forever.

If you own property, plan to buy, rent out homes, or hold property as part of retirement planning - now is the time to:

Review cash flow, mortgage cost, rental yields or property income projections

Run “what-if” scenarios (rate changes, tax rises, income fluctuations)

Evaluate whether property remains the right asset class for your goals or whether diversification makes sense

Ensure property plans are aligned with retirement, savings, pensions and wider financial goals

Pre-Retirement (in your 50s / early 60s)

What might change for you

Pension salary-sacrifice cap may reduce long-term pension growth if you're midway through building your pension pot.

Frozen thresholds could push more of your income into higher tax bands if wages or earnings rise.

The upcoming rise in the State Pension under the Triple Lock is good news - but depending on your private pension provision, you’ll need to factor in how the new rules alter your retirement income mix.

What to do now

Reassess pension contributions, considering both workplace pensions and private savings/investments.

Build a retirement cashflow plan - accounting for expected State Pension increase, private pensions, savings, and lifestyle costs.

Use this period to reduce debt (mortgages, credit), and increase more stable savings or investments for retirement years.

Consider seeking independent financial planning to structure your retirement savings optimally under the new rules.

Retirement Years

What might change for you

The 4.8% rise in State Pension from April 2026 offers a real-terms boost for pensioners.

However, rising taxes on savings, property income or dividend income as announced across some measures may affect returns if your retirement income relies on investments or rental income.

For those with existing pensions or investments, the value of careful asset allocation becomes even more crucial in a changed tax environment.

What to do now

Review your income mix - State Pension + private pensions + investments/rental income - and check how tax changes affect net income.

Rebalance investments, if needed, to manage tax exposure and income stability.

Consider using professional financial planning to optimise retirement income, factoring in inflation, tax, and changes to pension rules.

Why It Matters - And How Brancaster House Is Here for the Whole Journey

Life doesn’t stand still - and neither should your financial plan. The Autumn Budget 2025 underlines that what worked yesterday might need serious adaptation tomorrow.

At Brancaster House, we support individuals, families and business owners through every stage of life. Whether you’re starting out, scaling up, planning your exit, or navigating retirement - now is the time to review your plans in light of the changes.

We offer:

Holistic financial reviews

Pension strategy planning

Tax-efficient saving & investment advice

Retirement cashflow modelling

Business-owner and entrepreneur financial planning

With professional guidance, you can adapt to the new landscape - and steer your finances toward your long-term goals.

Comments